Insights and perspectives

Asset tokenization: Unlocking new opportunities for the investment sector

The tokenization of financial assets — and fund shares in particular — represents a defining shift in how savings and investment work, fundamentally changing the way assets are accessed, held, and transferred.

By converting traditional assets into digital tokens recorded on a blockchain, this innovation brings greater transparency, streamlined processes, and lower operational costs. For asset managers, distributors, and investors alike, it offers a powerful means to modernize financial infrastructure.

As initiatives continue to multiply across France and Europe, tokenization has firmly established itself as a strategic priority for the future of investment.

A regulatory environment that enables experimentation

Over the past several years, France and Europe have built a framework that both permits and secures experimentation with blockchain-based securities distribution and settlement. A key milestone was the French DEEP Ordinance of December 10, 2017, which legalized the use of Distributed Electronic Recording Devices for financial securities held outside of a central depository — paving the way for registered ownership on private DLT ledgers.

At the European level, the DLT Pilot Regime, in effect since March 23, 2023, provides an experimental regulatory framework for blockchain-based market infrastructures.

Against this backdrop, France has seen the emergence of several distribution platforms leveraging blockchain for fund register keeping.

IZNES runs a marketplace on a private blockchain connecting over sixty asset managers, with strong uptake from life insurers. FundsDLT, now integrated into Clearstream Fund Services, supports asset managers such as Ostrum, UBS AM, and Azimut in distributing their funds on-chain. SPIKO, a niche newcomer targeting corporate cash management through fully tokenized registered money market funds in multiple currencies, stands out for its reliance on public blockchains.

On the asset manager side, BNP Paribas Asset Management launched a tokenized share class of its money market fund in May 2025, distributed via DLT through Allfund (recently acquired by Deutsche Börse), while Amundi introduced last December a hybrid subscription option for its Amundi Funds Cash EUR money market fund — accessible through CACEIS via traditional channels or via blockchain tokenization.

Custodians are keeping pace with asset managers in this space. CACEIS Digital Assets has taken a leading role in tokenized funds and on-chain custody on public infrastructure (Ethereum), while BPSS explored earlier this year the use of a public blockchain to maintain the register of a BNP Paribas AM tokenized money market fund, in connection with BNP Paribas CIB’s Asset Foundry platform.

These developments make clear that the industry’s major players have fully embraced this shift — and have now mastered not only the technology itself, but also the operational complexities that come with it.

Three operational models, three adoption paths

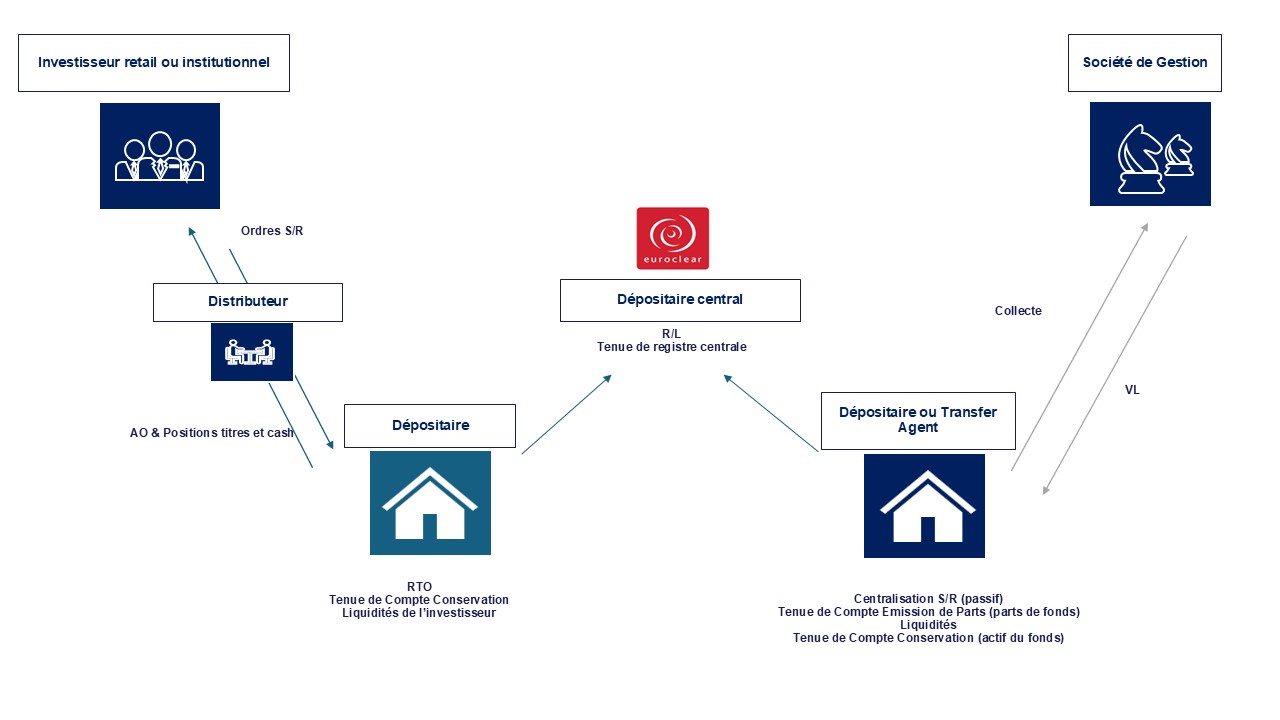

1. The traditional CSD-centric model

This model remains the gold standard in terms of reliability. The investor’s custodian bank handles order routing, settlement and delivery, and asset safekeeping. The fund depositary, acting under delegation from the asset manager, centralizes subscriptions and redemptions and maintains the fund’s share issuance account.

The Central Securities Depository (CSD) plays a pivotal role in the settlement and delivery process, as well as in maintaining the fund share register on behalf of local depositaries.

While this model offers a battle-tested processing chain, it is inherently complex — involving multiple layers of intermediaries such as global custodians, sub-custodians, and clearing houses — and falls short when it comes to cross-border interoperability, as illustrated by the fragmentation between systems like ESES and Euroclear.

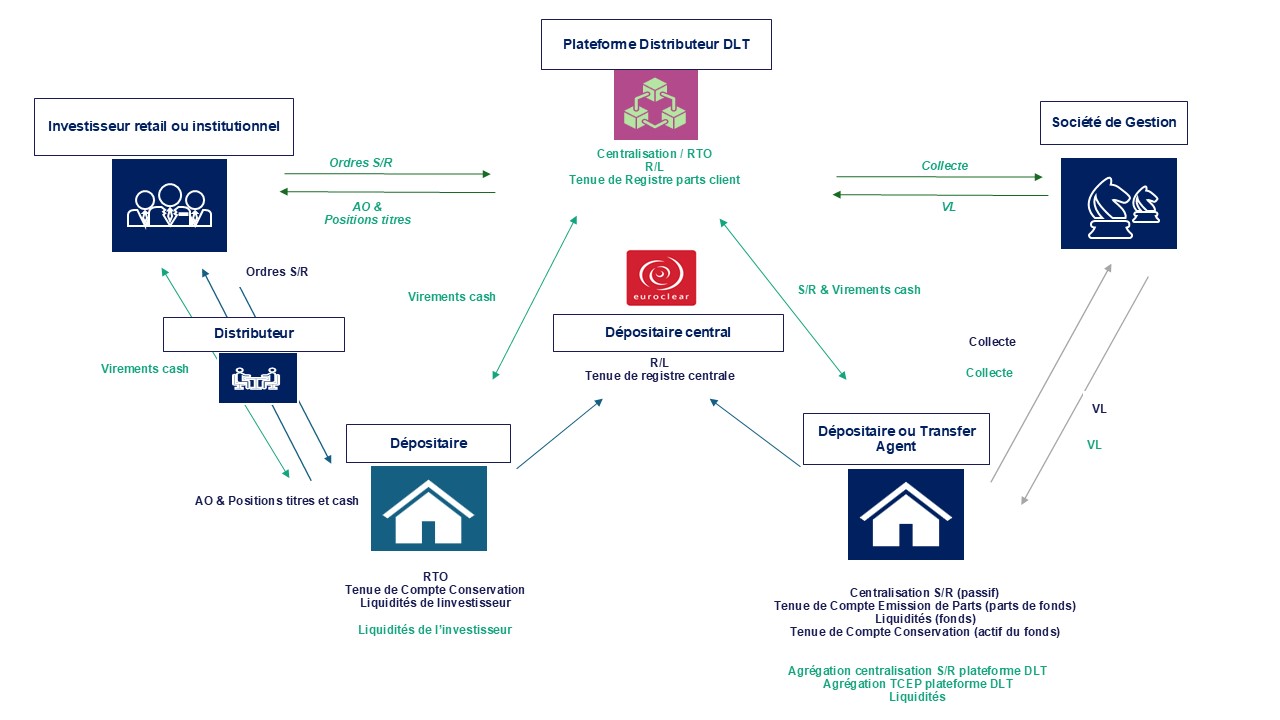

2. Hybrid Funds: A stepping stone between the traditional model and full tokenization

The hybrid model introduces a DLT platform as an additional distribution channel for the asset manager. Once an investor has been onboarded onto the platform — covering KYC and client profiling — the platform centralizes their orders acting as an order routing provider (RTO), handles settlement and delivery using the banking mandates granted by the investor, and finally records the fund shares in registered form on its own distributed ledger, typically a private blockchain.

The fund depositary, for its part, aggregates subscription and redemption requests coming from both traditional channels and the DLT platform, thereby maintaining a consolidated view of the fund’s liabilities. This model is particularly well-suited for institutional investors and asset managers looking to pilot DLT technology without disrupting their existing operational workflows.

For retail investors, the hybrid model offers a first taste of subscribing to funds through a blockchain-based distribution platform, but it stops short of genuinely transforming the client experience. Investors can still subscribe the way they always have, through their bank, or alternatively through the DLT platform they have previously registered on. The added value remains limited, however, since the client’s overall wealth picture becomes fragmented between their bank and the platform’s ledger — and the assets fall outside the tax-advantaged PEA wrapper.

In the context of life insurance contracts, the hybrid model is essentially neutral for the retail client. The subscription process is entirely managed by the insurer, who selects the distribution channel — CSD or DLT — without any impact on the client journey. The private bank retains a consolidated view of the client’s holdings regardless of which channel is used, meaning the end client notices no meaningful difference in their day-to-day experience. The real winner here is the insurer or the bank, which optimizes its operational chain — cutting costs, reducing processing times, and streamlining reconciliations — all without changing anything from the client’s perspective.

Institutional players — corporates, treasurers, and life insurers — stand to gain considerably more from the hybrid model, thanks to economic and operational levers that are more directly actionable.

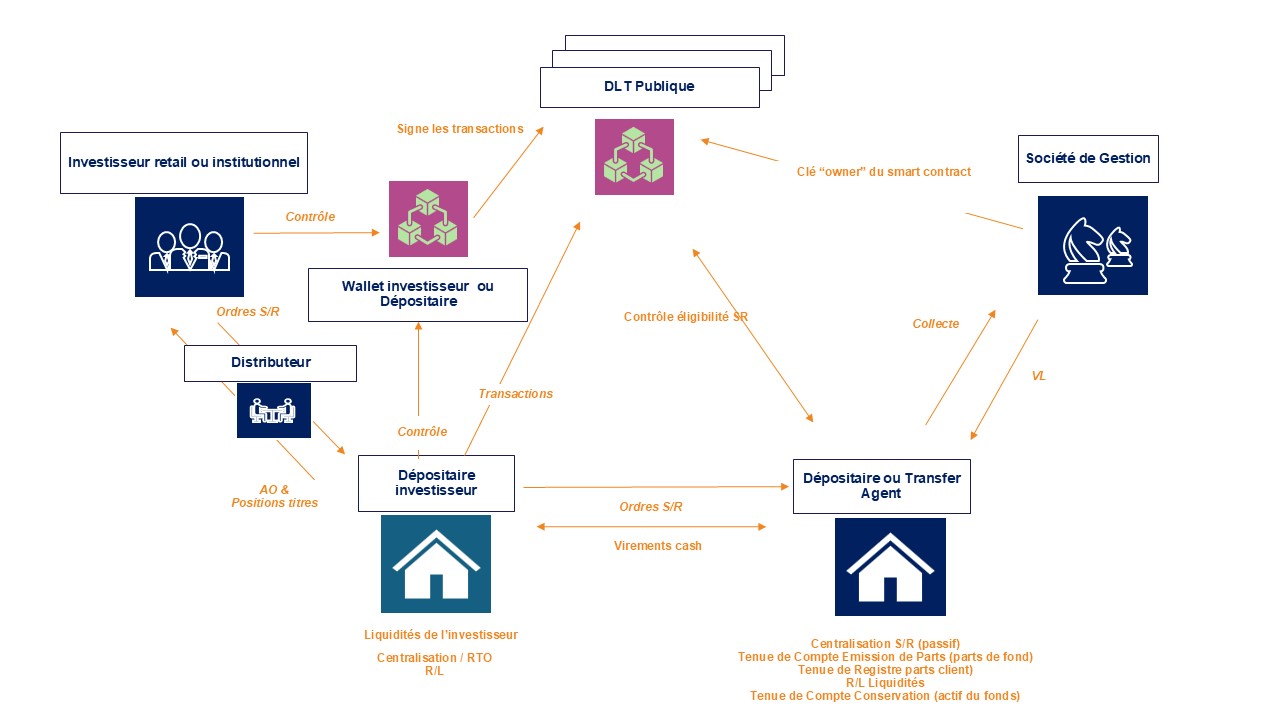

3. Fully Tokenized Funds: A deeper shift, driven by institutional players

The fully tokenized fund model takes things a step further by moving registered ownership entirely onto public DLTs (Ethereum, Polygon, Starknet, etc.), with fund shares issued exclusively by the asset manager in token form.

In practice, the investor provides the distribution platform or their custodian with a wallet address that has been pre-approved (allowlisted) in the fund’s smart contract. The platform or custodian then generates the on-chain transactions and signs them on behalf of the client using the private key associated with their wallet, before triggering the settlement and delivery process directly on the blockchain.

Once the transaction is finalized, the shares are permanently assigned to the client’s wallet. The asset manager maintains the register directly on the public DLT, accessible through their custodian.

With fully tokenized funds, the entire post-trade chain becomes simpler and largely automated: issuance, register keeping, transfers, settlement and delivery, and reporting all run directly on a shared digital infrastructure.

This approach is more ambitious than the hybrid model — it shifts the central register onto the blockchain and fundamentally redefines the role of intermediaries.

For retail investors, subscribing to fully tokenized fund shares requires holding a wallet to secure their asset keys.

In the life insurance context, however, the fully tokenized model has no direct impact on the retail client. The insurer remains the subscriber, and the client’s bank already has a complete view of their holdings regardless of the underlying model. Tokenization is, in effect, invisible to the end client.

For institutional investors, the fully tokenized model delivers on its promise more completely than the hybrid approach — driving down costs through a simplified post-trade chain and natively automated processes.

In summary, while the supply of fully tokenized fund shares remains very limited at this stage, this model is clearly the most efficient and most promising. The operational, financial, and strategic gains it offers are markedly superior to the hybrid model. Broader adoption now hinges on technological familiarity across the industry and on achieving interoperability between banks and DLT platforms.

What will accelerate over the next 12–24 months

The most realistic path forward for the market combines a hybrid transition phase — which allows organizations to learn and adapt — with a gradual convergence toward tokenized models in the segments where value creation is greatest, particularly among institutional investors.

For retail clients, the key priorities remain building familiarity with the technology, simplifying the overall experience (unified KYC, integrated custodial wallets), and enabling consolidated wealth management views.

For banks and fund distributors, the most critical investments will be in DLT platform interoperability, process automation and industrialization, and readiness for CBDC-based settlement environments.

About the author

-

![]() Jérôme BARIL Directeur

Jérôme BARIL DirecteurJérôme dispose d’une expérience de plus de 15 ans dans des missions de stratégie, organisation et pilotage de projet pour le compte d’Asset Managers, Banques Privées et Compagnies d’Assurance Vie en France et au Luxembourg

contact@valthena.com