Insights and perspectives

Life Insurance: Which Operational Model to Maximize the Performance of the General Fund in 2026?

The General Fund: A Strategic Asset at the Heart of Challenges

In 2026, the general fund of a life insurer stands as an essential lever of performance, a strategic pillar of differentiation, and a subject of increasingly stringent regulation.

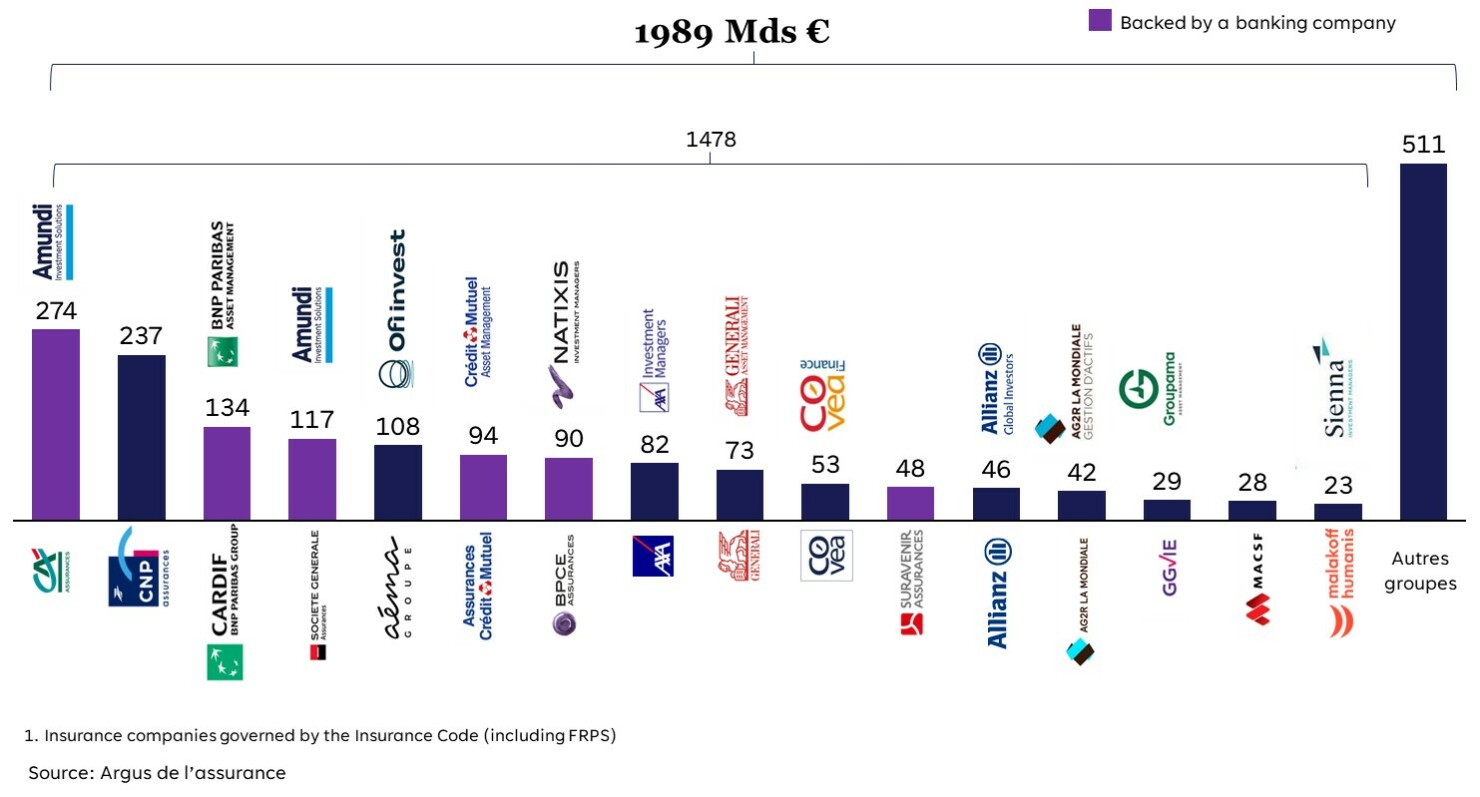

With over 70% of the €1,982 billion in assets under management in the French life insurance market by the end of 2024 (according to France Assureurs), the general fund concentrates most of the financial margins in the sector. The net yield, generally ranging between 2.5% and 3.5%, remains a decisive factor for savers, especially during periods of persistent volatility in unit-linked accounts (UC).

For insurers, the challenge lies in organizing management to optimize performance while adhering to prudential constraints (Solvency II, IFRS 17) and meeting expectations for sustainability and transparency.

Three operational models structure this choice: fully internalized management, outsourcing via mandates, and a mixed model. In all cases, the operational model must function as an agile execution mechanism, supported by clear governance and robust “data” architecture.

Total assets under management in life insurance in France at the en of 2024 in billion euros (€)

Why Is the General Fund at the Center of Tensions?

The general fund embodies the promise of capital security while being the primary source of profitability for a life insurer. Its performance relies on:

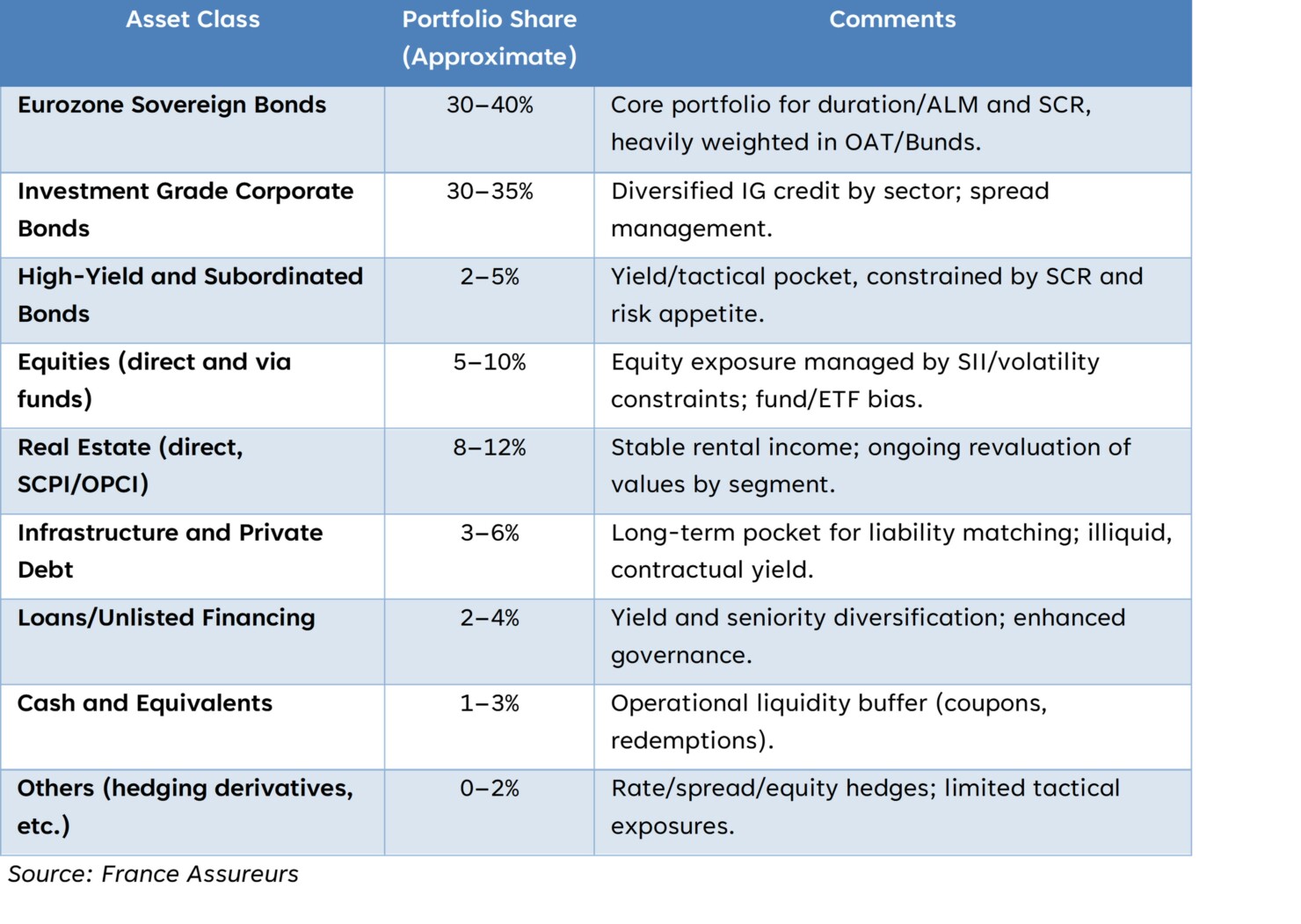

- A manageable allocation where the “investment grade” bond component remains central, complemented by real/private assets and disciplined cash management.

- Fine-tuned duration management to align with liabilities and stabilize the Other Comprehensive Income (OCI).

- Increased transparency of net returns and regularity.

The competitive battle now revolves around the speed of reinvestment (typical internal target: less than 5 days to recycle coupons, maturities, and cash flows), liquidity management (calibrated buffers, repo facilities, and securities lending), and the integration of sustainability criteria.

On this last point, the SFDR and Taxonomy regulations impose obligations for transparency and measurement. Alignment percentages (e.g., 30%) are internal objectives to be published, not a uniform regulatory quota.

Standard split by asset class

Two Operational Models – Strengths, Limitations, and Use Cases

Internalized Management – The Insurer as Master of the Game

This model suits players with strong management maturity and dedicated teams. It maximizes ALM control, allows near real-time duration adjustments, and synchronizes balance sheet arbitrages and hedging while maintaining strategy confidentiality. Efficiency gains often translate into compressed reinvestment times (e.g., 48 hours under normal conditions) and cost reductions.

However, it requires sustained investment in skills and systems:

- Internal expertise must cover ALM, rate/credit management, equity/alternative management, cash/margin management, execution, data, and SII/IFRS compliance.

- The necessary front-to-back application architecture includes an OMS/PMS for execution, a risk engine for SCR and stress tests, a treasury platform for buffers and margin calls, and a data hub ensuring references, look-through, and data quality.

- Strict governance separates decision-making, control, and execution, with a formalized RACI and scheduled committees.

Internally, insurers often target controlled OCI volatility (< 0.5%), prudential closing times of less than 5 days, and data error rates below 0.1%.

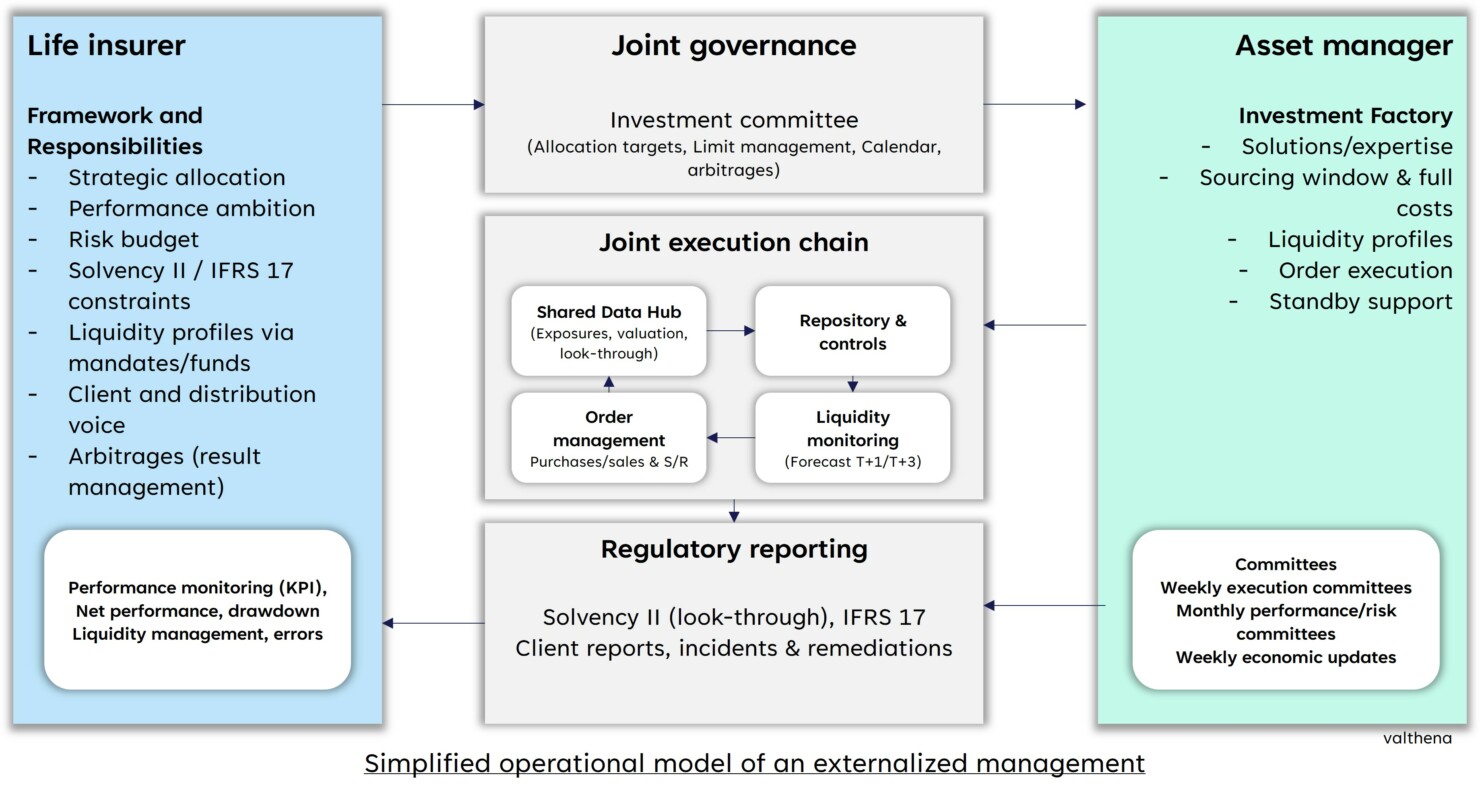

Mixed Model – Combining ALM Control and Access to Expertise

The mixed model is widely acclaimed by medium-sized insurers and transforming groups. The logic is to retain critical ALM pockets internally—core IG bonds, duration/hedging, cash, and buffers—while delegating high-barrier-to-entry classes such as real estate/infrastructure, private credit, or certain global themes. The indicative split is often 50–70% internal and 30–50% mandates, adjusted based on liabilities and organization.

Success in this model requires unified and scheduled governance, a clear RACI, crisis-tested playbooks, and a bimodal IT architecture: internal execution tools, connectors to asset management firms, and a shared data hub consolidating exposures and flows in near real-time.

A liquidity control tower anticipates needs over T+1/T+3/T+10 horizons and orchestrates buffers and facilities (repo, securities lending).

Simplified target operating model in a mixed model

Cross-Cutting Challenges – Skills, Organization, Systems

Regardless of the model, three challenges stand out:

- Skills: Attracting and retaining rare profiles such as ALM actuaries, bond traders, cash managers, data managers, and ESG experts, with continuous training plans and retention mechanisms tied to general fund performance.

- Organization: Clear separation of decision-making, control, and execution, supported by a common policy book (SAA/TAA, limits, KPIs, escalation rules), quarterly strategic committees, monthly risk/performance reviews, and weekly execution/liquidity meetings, plus ad hoc crisis mechanisms.

- Systems: Internal management requires OMS/PMS, risk engines, treasury platforms, and data hubs; mandate supervision demands a control data hub, shared references, and automated reporting; the mixed model imposes a bimodal architecture and a liquidity control tower.

Toward an Agile, High-Performing, and Compliant TOM

In 2026, the choice of an operational model for the general fund is not a binary decision between internal management and outsourcing but the construction of an ecosystem tailored to each insurer’s constraints and ambitions. Whether opting for integrated management, a mixed model, or selective outsourcing, the challenge is to drive performance with agility, aligning organization, skills, and systems with strategic objectives.

Two key points emerge for successful transformation:

- Adaptability: TOM must evolve based on internal resources, regulatory requirements (Solvency II, IFRS 17, SFDR), and market dynamics.

- Operational Performance: This relies on rigorous governance (clear RACI, scheduled committees) and robust data architecture capable of ensuring information quality, arbitration responsiveness, and yield transparency.

The goal? Transform the general fund into a lever of differentiation, where ALM mastery, execution speed, and ESG integration become competitive advantages. In an environment marked by volatility and growing sustainability expectations, the TOM is not an end but a driver of resilience and value creation, continuously adjusted to meet future challenges.

About the author

-

![]() Manuel PRESLIER Senior Manager

Manuel PRESLIER Senior ManagerManuel a une expérience de plus de 15 années dans le secteur de la banque et de l’assurance sur la gestion de programmes de transformation sur l’ensemble de la chaîne de valeur des actifs financiers (assurance-vie, gestion d’actifs, services de titres)

contact@valthena.com