Insights and perspectives

Digitalization of Savings Journeys : Which level of maturity ?

The digitalization of customer journeys in the French savings sector has accelerated sharply over the past five years. All market participants—online savings platforms, branch-based wealth banks, independent financial advisors (IFA), private banks and life insurers—now integrate digital solutions across every stage of the customer lifecycle.

However, digital maturity and the associated challenges vary significantly across players.

1. Savings journeys: different realities by use case (B2C vs. B2B)

It is essential to distinguish between two types of journeys depending on the nature of the players and the relationship model:

B2C journeys – platforms addressing end clients directly (e.g., online platforms, banks or life insurers)

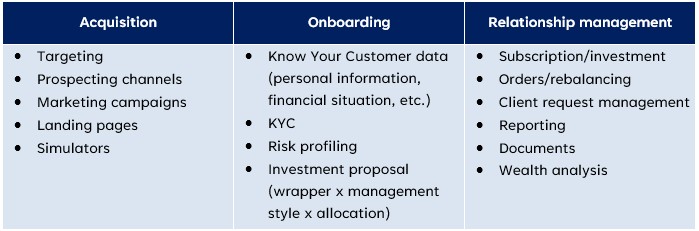

B2C journeys revolve around three main phases: acquisition, onboarding, and relationship management.

B2B journeys – platforms serving intermediaries (e.g., platforms provided by life insurers for CGPs or private banks)

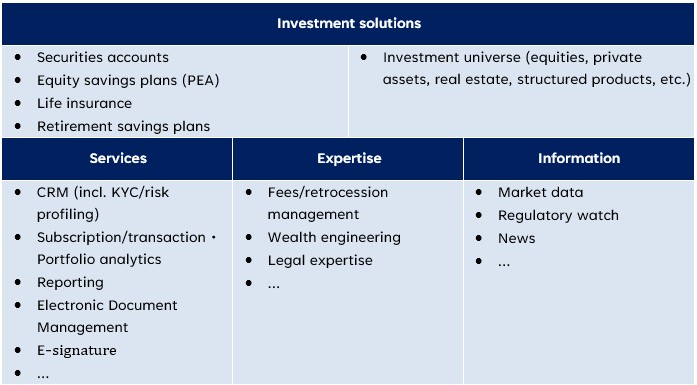

B2B journeys consist of services clustered into four categories: investment solutions, services, expertise and information.

2. Varied levels of digital maturity across market players

Online savings platforms: the “pioneers” of end‑to‑end digital journeys

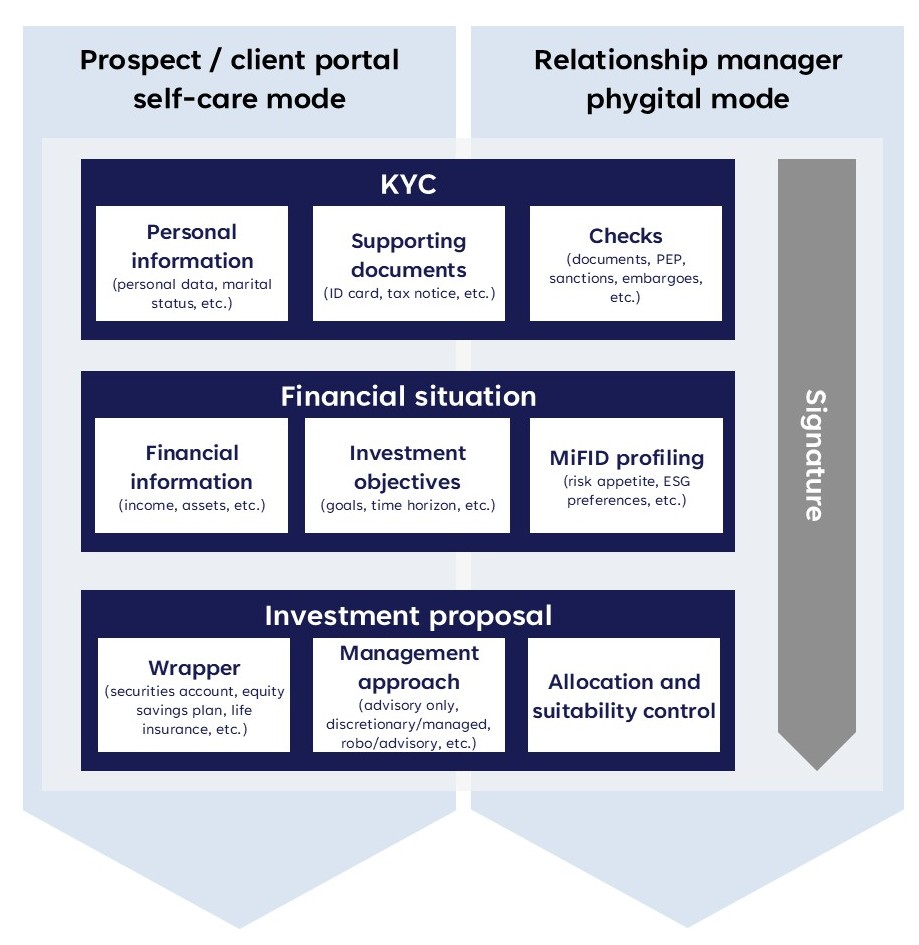

FinTech and online savings platforms display the highest degree of digitalization. Pure players such as Yomoni or Nalo offer fully dematerialized wealth management: client discovery, financial situation, client profiling, robo‑advised guided subscription, onboarding, realtime monitoring in the app, and digital signatures.

Yomoni surpassed €2 billion in assets under management in early 2026, evidence that these digital journeys now appeal to a significant number of savers—both younger, tech‑savvy segments drawn by ease of use and clients underserved by traditional banks.

To remain competitive, these platforms continuously innovate on UX and functionality. Finary, for example, provides a consolidated wealth view (aggregation of bank accounts, savings, life insurance, real estate, private equity) enriched with personalized analytics and educational content (including their YouTube channel with over 700,000 subscribers).

Overall, pure players set very high digital standards (subscription in minutes, polished mobile interfaces, 24⁄7 availability), pulling the entire market toward greater digitalization and simplicity.

Branch‑based wealth banks: porting retail banking’s digital standards into investing

Branch‑based wealth banks benefit from leveraging technology components built for day‑to‑day retail banking. By capitalizing on already‑covered services, they enrich savings journeys to deliver a premium client experience while aligning with the standards established by everyday banking apps.

Automated advisory modules are becoming widespread within apps: engaging MiFID questionnaires, risk scoring, model portfolios aligned to client profiles, and scheduled rebalancing. Journeys offer “turnkey” portfolios (profiled or thematic, often ESG) within life insurance and equity savings plans, with transparency on costs and risks.

For instance, SG Private Banking, together with startup Kwiper, has deployed a wealth, legal and tax diagnostic service powered by the “Mon Patrimoine” platform, enabling in‑depth discussions on wealth structuring and succession planning. Similarly, LCL has launched a “Mon Patrimoine” platform offering wealth aggregation, property valuation and simulators.

These capabilities support a resolutely phygital model, combining self‑service access with direct advisor interaction.

Independent financial advisors: from lag to a “digital leap”

Historically reliant on largely paper‑based processes, the CGP profession is undergoing profound transformation. This shift is driven by a tightening regulatory framework (MiFID II, GDPR, IDD) and a generational renewal of connected clients. In fact, 83% of CGPs observe greater autonomy and digital adoption among a new, active and dynamic clientele with different habits and expectations (BNPP Cardif CGP Barometer).

CGPs face a dual challenge:

- Equipping themselves with digital solutions to manage relationships with partners (private banks, life insurers). Many platforms exist in the market and are provided by life insurers or private banks within a “captive” partnership model.

- Equipping themselves with digital solutions for their end‑client relationship. On this front, CGP networks are investing heavily in proprietary tools or leveraging partners’

This evolution is reflected in the widespread adoption of e‑signature and videoconferencing, now firmly embedded in review meetings. Firms are investing heavily in platforms to automate compliance and gain a holistic wealth view. However, usage remains primarily focused on automating repetitive administrative tasks for 79% of CGPs.

Private banks: a resolutely “phygital” approach to personalize client relationships, while needing to meet market standards

Private banks have long prioritized human contact and bespoke processes, which initially slowed the digitalization of client experience. Yet client demand for digital is strong. Nearly one in two private‑bank clients will turn to digital within two years, with growing interest in the sector’s digital pure players (Simon‑Kucher Barometer).

In response, private banks are ramping up technology investment, often with the support of fintech partners.

All major brands have revamped or launched mobile apps for wealth clients and modernized websites with secure access to portfolios and documents.

The preferred model is “phygital”: these banks combine self‑care tools (consultation, subscriptions, e‑signature, secure vaults, alerts) with direct access to advisors.

Life insurers: the maturity age of extranets

In the wealth life insurance segment, the past decade has seen a gradual shift from paper to digital processes.

Some insurers are also embracing the phygital turn—such as CA Assurances with Oriance — offering life insurance products that clients can subscribe to entirely autonomously via the app, while retaining the option to engage with an advisor.

For intermediaries, most insurers provide CGPs, brokers and private banks with a portal where they can create prospects, have subscription forms completed and signed online, track policies, view up‑to‑date client assets, execute portfolio switches and partial surrenders, and access all contractual and tax documents.

For example, Vie Plus (Suravenir) enables, via its extranet, the automation of administrative tasks previously performed manually—such as data entry and dossier completeness checks—freeing CGP partners to focus more on advice.

Other life insurers are launching platforms dedicated to interactions with CGPs and aimed at simplifying their work—for instance, AXA with the launch of AXA Wealth Digital (digital subscription journeys with e‑signature, integrated KYC, online switches, advisory modules, simulators, etc.).

3. Digital journeys: trends and innovations

Acquiring new clients

Digital acquisition has become central to growing online savings. It relies on a simple, effective foundation: be visible, attract interest, qualify then convert.

Optimized SEO and SEA campaigns ensure visibility with the right audiences. Clear, engaging educational content—simulators, comparators, webinars, short videos—builds interest and credibility.

These initiatives capture initial data points which, combined with analytics tools, enable precise lead qualification and timely, channel‑appropriate recommendations.

Readable landing pages paired with a streamlined onboarding flow (few steps, inline explanations, e‑signature) reduce churn and accelerate subscription.

This approach is particularly effective with younger segments who value mobile, fast and educational experiences. Digital acquisition is thus a key lever to renew the savings client base.

Educational and personalized client spaces

Savings client spaces are shifting toward an augmented relationship driven by three key trends.

First, personalisation through data and AI: inspired recommendation engines generate dynamic allocations and contextualised content, enhancing the relevance of advice and speed of decision-making. For example, BNP Paribas Wealth Management has launched Allocation Designer, a tool that allows users to interactively and visually simulate strategic allocation scenarios.

Second, aggregation for a 360‑degree view of wealth via open banking and components such as Bankin’/Linxo. Near real‑time, multi‑institution consolidation provides a single basis for wealth diagnostics and re‑allocations.

Finally, investment enablement through interactive dashboards, educational content and simulators (for example, retirement simulators).

B2B tools

Independent advisors rely on distributor extranets and multi‑provider platforms that centralize asset management. Modernisation efforts focus on tool interconnectivity, enabling automatic retrieval of policy valuations and eliminating manual reentries that cause errors. The sector’s future lies in data standardization, driven by the European FIDA regulation.

This easier sharing of financial information promises advisors a panoramic view of their clients’ wealth while streamlining compliance processes within an increasingly integrated ecosystem.

Conclusion

In five years, the French savings market has crossed a threshold: online subscription, mobile consultation and dematerialized transactions have become standard.

Yet the work is not done.

Maturity gaps persist, client expectations are rising, and data/AI orchestration, omnichannel capabilities and B2B/API industrialization will be the true differentiators. The next stage will hinge on three axes: simpler and safer journeys, genuinely useful personalization, and seamless integration between clients, advisors and partners.

Those who align vision, execution and speed will gain a lasting edge.

.

About the authors

-

![]() Nicolas CHAPIS Associé

Nicolas CHAPIS AssociéRiche de 25 années d’expérience professionnelle dans le conseil, Nicolas met son expertise dans la gestion de programmes de transformation complexe à dominante stratégique, règlementaire ou opérationnelle au service des acteurs du wealth management, de la gestion d’actifs et de la banque de financement et d’investissement.

contact@valthena.com -

![]() Thomas SEVRAIN Senior Manager

Thomas SEVRAIN Senior ManagerThomas intervient dans les domaines de la banque privée en apportant son expertise dans les domaines de la distribution et de la relation client.

contact@valthena.com